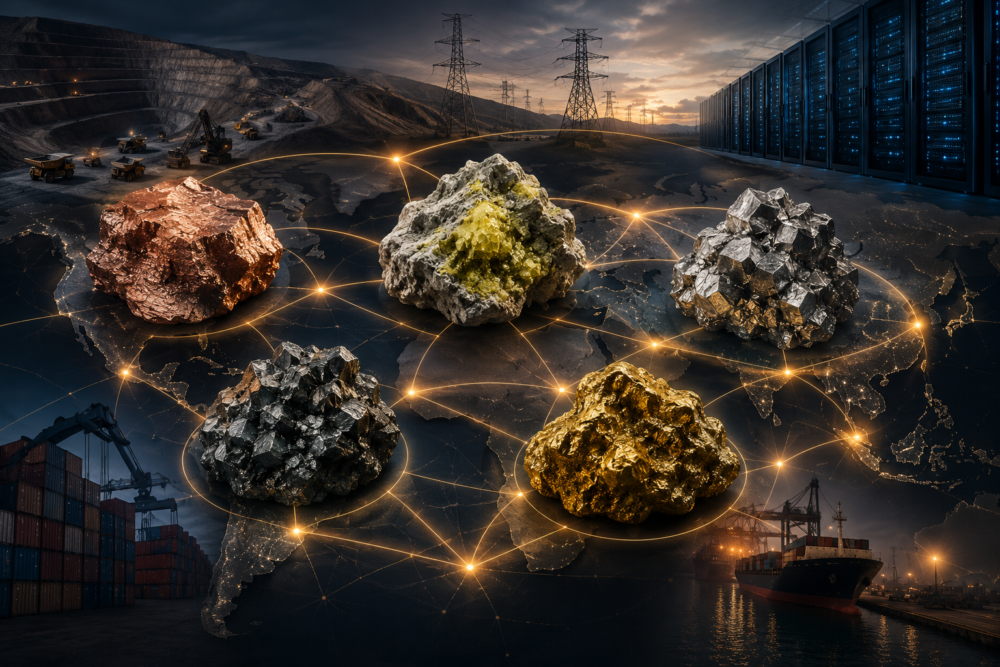

Critical minerals have moved beyond their traditional role as industrial commodities.

Today, they sit at the centre of a global competition driven by national security, artificial intelligence, clean energy and advanced manufacturing. Governments increasingly view reliable access to these resources as a strategic priority, while investors have begun treating them as long-term growth opportunities rather than cyclical mining plays.

The shift reflects a changing global economy. Copper, uranium, rare earth elements, lithium and antimony now support technologies ranging from electric vehicles and renewable energy systems to advanced weapons, robotics and hyperscale data centres. As demand grows, countries are also rethinking where those materials come from and who controls their supply chains.

Consequently, governments have expanded financial support for new mines, processing facilities and refining capacity. They have also accelerated permitting reforms, strengthened domestic supply chains and encouraged partnerships with allied nations. Meanwhile, geopolitical tensions have shown the risks of relying on a small number of suppliers for materials essential to economic and military security.

The mining industry has responded by adapting its priorities. Exploration companies are pursuing deposits offering strategic value alongside strong economics. In addition, producers are expanding projects that can help diversify global supply. Investors have also shifted their attention beyond traditional battery metals as new sources of demand continue to emerge.

This roundup examines five trends reshaping the critical minerals industry.

China is rerouting global supply chains

China’s dominance of the global critical minerals supply chain has become one of the biggest catalysts reshaping the mining industry. While many countries possess significant mineral deposits, China has spent decades building an unmatched refining and processing network. Today, it controls most global rare earth processing capacity and remains a leading supplier of materials essential for semiconductors, defence systems, electric vehicles and advanced manufacturing. Consequently, governments around the world have become increasingly concerned about the concentration of supply.

Those concerns have intensified as Beijing has expanded export controls on key materials, including gallium, germanium, antimony and several rare earth elements. As a result, governments and manufacturers have accelerated efforts to secure alternative sources outside China.

The shift has given rise to “friend-shoring,” a strategy prioritizing sourcing critical materials from trusted allies instead of geopolitical rivals. Countries including the United States, Canada and Australia have expanded partnerships to develop new mines, processing facilities and manufacturing capacity while reducing dependence on Chinese supply chains. The approach has also attracted growing investment into companies positioned to become alternative suppliers.

Among the beneficiaries is MP Materials (NYSE: MP). This company operates the only active rare earth mine and processing facility in the United States. Meanwhile, Lynas Rare Earths (ASX: LYC) (OTCMKTS: LYSDY) has become one of the largest rare earth producers outside China, supplying manufacturers seeking diversified supply chains.

Read more: NevGold pushes toward potential 2027 antimony production at Limousine Butte

Read more: NevGold reports more positive drill results as gold-antimony resource estimate nears

Governments are funding mines instead of waiting for markets

Governments have responded to growing supply chain risks by taking a more active role in developing domestic critical minerals industries. Policymakers are increasingly providing loans, grants and regulatory support to accelerate new mining and processing projects. The goal extends beyond economic growth. Many countries now view secure access to critical minerals as essential to national security, energy independence and technological leadership.

In the United States, federal agencies have expanded financial backing for strategically important projects through the Department of Defense and Department of Energy. Loan guarantees, grants and strategic investments have helped companies advance projects involving rare earth elements, antimony, lithium and other critical materials. Meanwhile, the FAST-41 permitting initiative aims to streamline environmental reviews for major infrastructure and mining projects without eliminating federal oversight.

The policy shift has already benefited several publicly traded companies. Perpetua Resources Corp (TSE: PPTA) (NASDAQ: PPTA) secured significant federal support for its Stibnite project in Idaho, which could become one of the largest domestic sources of antimony while also producing gold. Similarly, Lithium Americas Corp (TSE: LAC) (NYSE: LAC) (FRA: WUC) has received government backing for the Thacker Pass project in Nevada as Washington works to strengthen North American battery supply chains.

Canada has adopted a similar approach through its Critical Minerals Strategy. It has committed billions of dollars to infrastructure, exploration, processing capacity and Indigenous partnerships. Export credit agencies and strategic investment funds have also increased financing for projects capable of supplying allied nations with reliable sources of key minerals.

Defence is becoming the next demand supercycle

Defence demand has become one of the strongest new forces reshaping the critical minerals industry.

Military supply chains now depend on a much wider group of specialized materials. Antimony is used in ammunition, flame retardants and some battery technologies. Tungsten supports armour-piercing projectiles, cutting tools and high-temperature applications. Rare earth magnets are essential for guidance systems, drones, radar and electric motors. Titanium remains important for aerospace, naval systems and advanced military hardware.

The shift has changed how investors and governments evaluate mineral projects. A deposit no longer needs to fit neatly into one commodity category to attract attention. Instead, exploration companies are increasingly showcasting projects that combine precious metals, base metals and strategically important critical minerals. That has created new opportunities for juniors originally focused on gold, silver or copper.

NevGold Corp (CVE: NAU) (OTCMKTS: NAUFF) (FRA: 5E50) offers one example through its Limousine Butte project in Nevada. The company has primarily advanced the project as a gold asset. However, recent work has also identified antimony mineralization. This gives the project added relevance as Western governments search for domestic sources of defence-linked minerals.

Other companies are following similar paths. Military Metals Corp. (CNSX: MILI) (OTCMKTS: MILIF) has focused more directly on antimony assets.

Read more: NevGold Corp. reports antimony grades up to 53.7 per cent at Nevada project

Read more: NevGold raises up to CAD$25M to fast-track Limo Butte development

AI is changing the mining industry

Artificial intelligence has become one of the mining industry’s newest demand drivers. However, the opportunity extends well beyond AI software. Every large language model, cloud platform and hyperscale data centre depends on enormous amounts of electricity, creating growing demand for the raw materials needed to generate, transmit and distribute power.

Copper sits at the centre of that trend. The metal is essential for power cables, transformers, substations and transmission lines that connect new generating capacity to expanding data centre networks. Silver also plays a key role through its exceptional electrical conductivity, making it valuable for electronics, power systems and other high-performance applications. As utilities race to modernize aging grids, demand for both metals is expected to remain strong.

The need for reliable, around-the-clock electricity has also renewed interest in nuclear energy. Unlike wind and solar power, nuclear reactors provide consistent baseload generation capable of supporting energy-intensive AI workloads. That has strengthened the long-term outlook for uranium as governments and technology companies seek dependable, low-carbon power sources for future computing infrastructure.

Several publicly traded companies are already positioned to benefit from those trends. Cameco Corp. (TSE: CCO) (NYSE: CCJ) remains one of the world’s largest uranium producers as countries expand nuclear generation. Meanwhile, Freeport-McMoRan Inc. (NYSE: FCX) continues to supply copper for electrical infrastructure needed to support growing electricity demand. Rather than replacing traditional mining, artificial intelligence is reinforcing the importance of the industry’s foundational commodities. Every new data centre ultimately requires more electricity, more transmission infrastructure and more critical minerals to keep the digital economy running.

Exploration is becoming more strategic

The criteria used to evaluate mining projects have expanded alongside changing geopolitical priorities. Companies are increasingly examining whether a deposit can contribute to domestic supply chains, support strategic industries and reduce reliance on overseas processing. Those considerations now sit alongside more traditional measures such as grade, size and project economics.

Many exploration companies are also highlighting deposits containing multiple commodities rather than a single target metal. Projects combining gold with antimony, copper with silver or rare earth elements with other critical minerals may attract broader interest from investors and governments seeking diversified sources of supply. At the same time, developers are placing greater emphasis on domestic processing capacity instead of exporting raw materials for refining abroad.

Jurisdiction has also become a more prominent consideration. Stable regulatory environments, established infrastructure and predictable permitting processes can influence project development timelines and financing decisions. Environmental, social and governance practices also remain an important part of project planning, particularly as companies work with local communities and Indigenous partners throughout the permitting process.

Strategic partnerships have expanded across the sector as well. Mining companies are increasingly collaborating with governments, manufacturers and technology firms to strengthen supply chains from exploration through processing. For example, Rio Tinto Group (NYSE: RIO) has expanded its critical minerals portfolio through partnerships and acquisitions, while MP Materials is developing an integrated rare earth supply chain that includes mining, processing and magnet manufacturing in the United States.

NevGold Corp is a sponsor of Mugglehead news coverage

.